Property foreclosure in New York can feel complicated, especially when you look at how it works across different counties in 2026. Whether you are a homeowner trying to understand your rights or an investor looking for opportunities, knowing the full process is very important. New York follows a judicial foreclosure system, which means every foreclosure case must go through the court before a property can be sold.

This guide explains the New York foreclosure process, county-level variations, homeowner protections, and important tips for investors in a simple and clear way.

Understanding Property Foreclosure in New York

What is Foreclosure?

Foreclosure is a legal process where a lender (usually a bank or mortgage company) takes ownership of a property after the homeowner fails to keep up with mortgage payments or other financial obligations.

In New York, most foreclosures are judicial, meaning the lender must file a lawsuit in court before the property can be sold. In some cases, unpaid property taxes can also lead to tax foreclosure proceedings.

Why Foreclosures Happen

Foreclosure can happen for several reasons, such as missed mortgage payments, financial hardship, job loss, medical expenses, or unpaid property taxes. Sometimes rising living costs or unexpected life changes can push homeowners into default. Understanding these reasons helps both homeowners and investors better evaluate risks and options.

Legal Framework in New York

New York foreclosure laws are mainly governed by RPAPL (Real Property Actions and Proceedings Law). This law ensures that homeowners receive proper notice, legal protection, and an opportunity to respond before losing their property.

Although the process follows statewide rules, each county court handles filings, scheduling, and auctions based on its own workload and procedures. This creates slight differences in timing across counties.

New York Counties and Foreclosure Differences

New York has 62 counties, and foreclosure activity varies significantly across them. Urban counties tend to have higher volumes, while rural counties often move at a slower pace.

Examples of County Differences:

- Kings County (Brooklyn) – Very active foreclosure market with high investor interest and frequent court listings.

- Queens County – Large volume of residential cases, with structured court supervision and auction listings.

- New York County (Manhattan) – Fewer residential foreclosures but high-value commercial cases.

- Bronx County – High foreclosure activity due to dense housing market and economic pressure.

- Nassau County – Suburban market with steady foreclosure filings and strong buyer competition.

- Suffolk County – Long Island foreclosures often include single-family homes and longer timelines.

- Westchester County – Moderate activity with higher property values and stricter legal handling.

Understanding these differences helps homeowners act before deadlines and helps investors plan better strategies.

New York Foreclosure Statistics by County (Overview)

Foreclosure activity changes from county to county depending on economic conditions and housing demand.

| County | Foreclosures | Activity Level |

|---|---|---|

| Kings County | 150+ | High |

| Bronx County | 140+ | High |

| Queens County | 130+ | High |

| Suffolk County | 90+ | High |

| Nassau County | 80+ | Medium-High |

| Westchester County | 50+ | Medium |

| Erie County | 40+ | Medium |

| Monroe County | 35+ | Medium |

| Albany County | < 20 | Low |

Step-by-Step New York Foreclosure Process

Step 1 – Missed Payments & Default Notice

The process usually begins when a homeowner misses mortgage payments. After a certain period (commonly 90 days), the lender issues a default notice informing the borrower about the overdue amount and potential legal action.

Step 2 – Lis Pendens Filing

The lender files a Lis Pendens with the county clerk. This is a public notice that a foreclosure lawsuit has started, which also restricts the property from being sold or refinanced easily.

Step 3 – Foreclosure Lawsuit Filing

The lender officially files a foreclosure complaint in New York Supreme Court (county-level). The homeowner is served a summons and complaint and typically has 20–30 days to respond.

Step 4 – Response, Settlement & Possible Mediation

Homeowners may respond to the lawsuit, dispute errors, or enter settlement discussions. New York courts often encourage mediation programs to help avoid foreclosure through repayment plans or loan modifications.

Step 5 – Court Judgment

If no agreement is reached, the court may issue a judgment of foreclosure and sale. This allows the lender to proceed with selling the property through a public auction.

Step 6 – Foreclosure Auction

The property is sold at a public auction, often held by a referee appointed by the court. Many counties now publish auction details online. Buyers usually must pay in cash or certified funds.

Step 7 – After the Auction

The winning bidder receives a deed after court confirmation. In most New York mortgage foreclosures, there is typically no redemption period, meaning ownership transfers quickly after sale approval.

County-Specific Foreclosure Variations in New York

While the legal framework is statewide, counties handle execution differently:

- Kings County – High-volume court system; frequent auction listings.

- Queens County – Structured foreclosure calendar with heavy residential caseload.

- Bronx County – Faster-moving cases due to court efficiency and high demand.

- Nassau County – More homeowner defense activity and negotiation attempts.

- Suffolk County – Longer timelines due to suburban property reviews.

- Erie County (Buffalo) – Moderate foreclosure activity with steady auction flow.

- Monroe County (Rochester) – Balanced foreclosure filings with consistent court schedules.

Each county may also differ in how auctions are posted, how quickly cases move, and how strictly timelines are enforced.

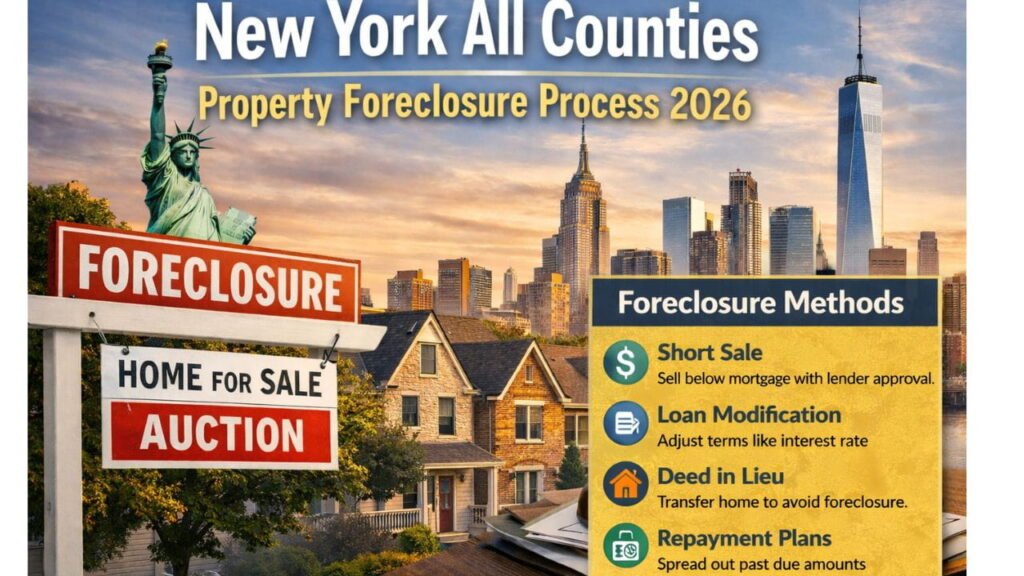

Foreclosure Alternatives for New York Homeowners

Homeowners facing foreclosure may still have options:

Short Sale

Selling the property for less than the mortgage balance with lender approval.

Loan Modification

Adjusting loan terms such as interest rate or payment schedule to make payments more manageable.

Deed in Lieu of Foreclosure

Voluntarily transferring ownership to the lender to avoid court proceedings.

Repayment Plans & Forbearance

Temporary arrangements allowing missed payments to be spread out or paused.

Tax Foreclosure in New York

Unpaid property taxes can also lead to tax foreclosure actions, depending on the county. Some counties may auction tax liens, while others proceed with full property foreclosure after extended non-payment periods. Investors should carefully study local county rules because redemption rights and timelines vary widely.

Protecting Homeowner Rights in New York

Homeowners are protected under New York law, including:

- Right to receive proper legal notice

- Right to respond in court

- Right to request mediation or settlement options

- Right to challenge incorrect charges or procedural mistakes

It is also important to avoid foreclosure scams by verifying all legal documents and court notices.

Tips for Investors in New York Foreclosures

Investing in foreclosure properties can be profitable, but it requires careful planning:

- Review county court records regularly

- Track auction schedules and updates

- Understand property condition and repair costs

- Check for liens, unpaid taxes, or legal issues

- Study neighborhood trends before bidding

- Be aware of bidding competition in high-demand counties

Conclusion

The New York foreclosure process in 2026 is structured but varies depending on the county. Since it is a judicial system, every case goes through the courts, ensuring legal protection for homeowners. However, timelines, auction methods, and case volume differ widely across the state’s 62 counties.

For homeowners, early action and understanding available alternatives can make a big difference. For investors, strong county-level research is the key to making informed and safe decisions in the foreclosure market.

Frequently Asked Questions (FAQs)

How long does foreclosure take in New York?

It usually takes 8 months to 2 years, depending on the county and court backlog.

Can foreclosure be stopped in New York?

Yes, homeowners can stop or delay foreclosure through repayment plans, loan modification, or court mediation.

Are foreclosure auctions public in New York?

Yes, auctions are public and often listed online by county courts or appointed referees.

Is there a redemption period in New York foreclosure cases?

In most mortgage foreclosures, there is no redemption period after the auction is completed.

Do foreclosure rules differ across New York counties?

Yes. While the legal process is the same statewide, timelines, court handling, and auction procedures can vary by county.